A Real Gamble Call Trade

This post documents a real options trade involving a short-dated call option. Within this trading journal, positions like these are labeled “Gamble Calls” to track speculative call purchases and evaluate how often they succeed or fail over time.

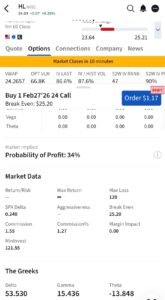

On February 23, 2026, a short-dated call option was initiated on Hecla Mining Company with an expiration of February 27, 2026.

The position was opened using:

-

Strike price: $24

-

Premium paid: $1.17

This established a break-even price of $25.17.

At entry, the option carried a delta of approximately 0.53, indicating moderate sensitivity to upward price movement. Theta was −13.8, reflecting rapid time decay due to the extremely short time remaining until expiration.

Despite expectations for near-term momentum, the underlying stock failed to advance sufficiently toward the break-even threshold. Even broader macro catalysts — including heightened market attention surrounding a presidential address from the White House — did not translate into meaningful price movement for HL. This outcome highlights one of the core risks of short-dated options: external news events do not always produce the price movement traders anticipate.

Opening the Gamble Call Position

The position was opened with the expectation that a short-term rally could quickly push the option into profitability. Short-dated calls can offer significant upside because small movements in the underlying stock can produce large percentage changes in the option’s value. However, the same leverage that creates opportunity also increases risk when the expected move fails to materialize.

Closing the Trade

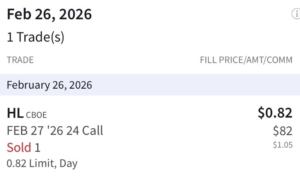

As expiration approached and the probability of a favorable move diminished, the position was closed on expiration day using a sell-to-close order at $0.82.

This resulted in:

-

Loss per contract: $0.35

-

Total loss: $35 (based on the 100-share contract multiplier)

With limited time remaining and insufficient momentum in the underlying stock, the statistical odds no longer supported maintaining the position. Rather than allowing the option to expire worthless, the decision was made to exit early and preserve remaining capital.

Why These Trades Are Called “Gamble Calls”

Trades like this are intentionally labeled “Gamble Calls” because single-leg call options often resemble lottery-style bets.

A relatively small premium can offer significant upside, but the probability of success is typically low. In fact, a large percentage of short-dated options ultimately expire worthless.

This does not necessarily mean the trade idea is wrong. For a short-dated option to succeed, three factors must align simultaneously:

-

correct price direction

-

sufficient price magnitude

-

precise timing before expiration

If any one of those variables fails, the trade often loses value rapidly.

Speculation vs. Reckless Gambling

Short-dated call buying can resemble gambling, but speculation itself is not automatically irresponsible.

When risk is predefined, consciously accepted, and properly sized, speculative trades can serve a specific purpose within a broader trading framework.

The key difference lies in risk control.

Impulsive bets expose traders to uncontrolled downside, while calculated speculation limits losses to a known amount while leaving room for asymmetric upside.

Growth rarely comes from avoiding risk entirely. Instead, successful traders focus on identifying situations where the potential reward justifies the limited and clearly defined downside.

Related Post: Are Options Gambling?

This Gamble Call example connects directly to a broader discussion about speculation in options markets. To explore the relationship between short-dated options and gambling behavior, read the related article:

That post examines whether buying calls and puts resembles gambling and how traders can approach speculative options trades in a more disciplined way.